We are committed to providing timely, high quality information to investor on the internet.

Investor Relations

Financials

Financials

Half Year Financial Statement And Dividend Announcement 2025

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

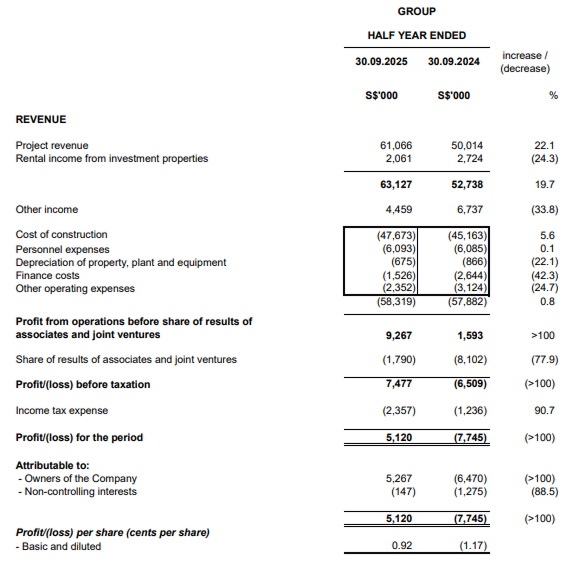

Condensed interim consolidated income statement

Condensed interim consolidated statement of comprehensive income

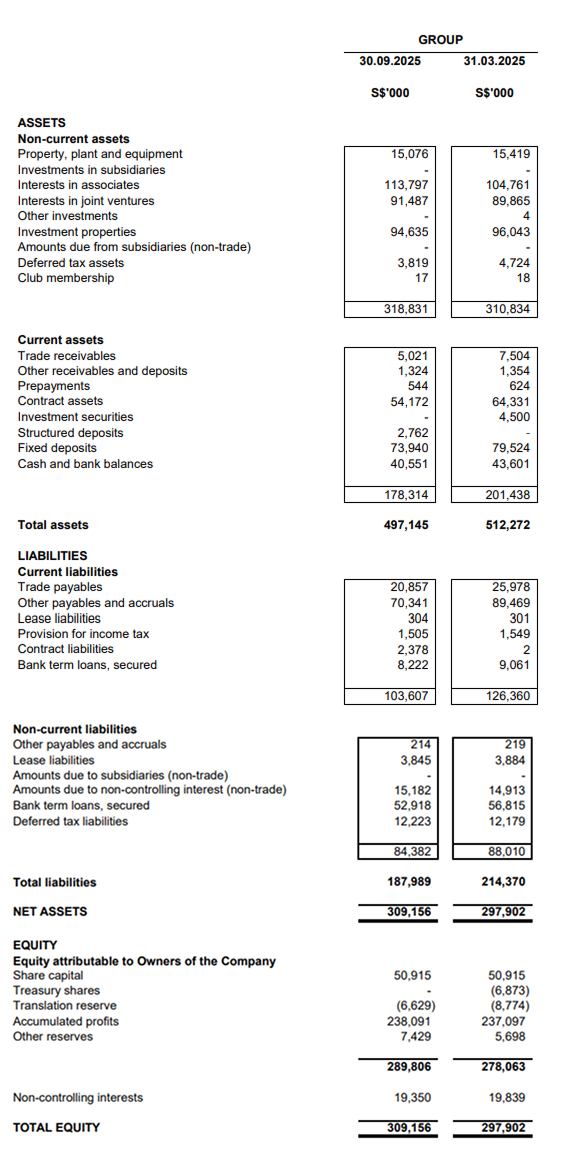

Condensed interim balance sheets

Review of Performance

Half year results : 1HFY2026 vs 1HFY2025

Revenue

The Group had a total revenue of S$63.1 million for 1HFY2026, an increase of S$10.4 million compared to S$52.7 million in the corresponding 1HFY2025. The increase was driven by higher revenue from the construction business, which rose S$11.1 million from S$50.0 million in 1HFY2025 to S$61.1 million in 1HFY2026. The growth in construction revenue was primarily due to the higher work progress achieved across ongoing projects. The decrease in rental income from investment properties was largely due to a lower exchange rate applied to rental income from the PRC.

Other income

The decrease in other income of S$2.2 million from S$6.7 million in 1HFY2025 to S$4.5 million in 1HFY2026 was due to the decrease in gain on disposal of plant and equipment of S$1.4 million and interest income of S$0.8 million.

Other operating expenses

Cost of construction increased by S$2.5 million from S$45.2 million in 1HFY2025 to S$47.7 million in 1HFY2026, which is in line with the higher construction revenue, the construction segment recorded an improvement in profit margin.

Finance costs decreased by S$1.1 million from S$2.6 million in 1HFY2025 to S$1.5 million in 1HFY2026 mainly due to lower gearing and reduced cost of borrowings.

Other operating expenses decreased by S$0.7 million from S$3.1 million in 1HFY2025 to S$2.4 million in 1HFY2026 was mainly attributable to a decrease in building maintenance expenses of investment property in PRC and utilities.

Share of results of associates and joint ventures recorded a loss of S$1.8 million, mainly arising from certain expenses and operating costs that were required to be fully recognised upon incurrence, while revenue recognition was limited by the percentage of completion of construction method, as these projects remained in the early stages of development in accordance with the adopted accounting standards.

Overall, the Group recorded a net profit attributable to owners of the Company of S$5.3 million in 1HFY2026 as compared to a loss of S$6.5 million in 1HFY2025 excluding non-controlling interests.

Group Statement of Financial Position Review

Non-current assets as at 1HFY2026 increased by S$8.0 million or 2.6% to S$318.8 million as compared to S$310.8 million as at FY2025 mainly due to the increase in interests in associates and joint ventures.

The net current assets (current assets less current liabilities) of the Group was S$74.7 million as at 1HFY2026 as compared to S$75.1 million as at FY2025.

Fixed deposits, cash and bank balances decreased by S$8.6 million from S$123.1 million in FY2025 to S$114.5 million in 1HFY2026 mainly due to repayment of banks borrowings and extension of additional shareholder's loans extended to associates and joint ventures, offset by proceeds from redemption of quoted debt instruments (investment securities) and sale of treasury shares.

Gearing ratio (total loans and borrowings to equity) of the Group has improved to 0.20x in 1HFY2026 from 0.22x in 1HFY2025 with a S$4.8 million decrease in total loans and borrowings from S$65.9 million as at FY2025 to S$61.1 million as at 1HFY2026.

Commentary On Current Year Prospects

According to the Monetary Authority of Singapore ("MAS"), the global economy has remained broadly resilient since the last monetary policy review. Advance estimates from the Ministry of Trade and Industry ("MTI") show that the Singapore economy grew by 2.9% year-on-year in the third quarter of 2025, moderating from the 4.5% expansion in the previous quarter. In the quarters ahead, global growth should moderate as front-loading activity dissipates while labour markets soften and spending slows. While core inflation could edge down further in the near term, some of the factors dampening inflation are expected to diminish in the quarters ahead. MAS Core Inflation is forecast to average around 0.5% for 2025 as a whole and come between 0.5% and 1.5% in 2026.

According to MTI, Singapore's construction sector grew by 3.1% year-on-year in the third quarter of 2025, moderating from the 6.2% growth recorded in the preceding second quarter. Growth was supported by an increase in both public and private sector construction output. On a quarter-on-quarter seasonally-adjusted basis, the sector contracted by 1.2%, a reversal from the 6.5% expansion in the second quarter of 2025.

According to the Urban Redevelopment Authority ("URA"), the overall private residential property price index rose by 0.9% in the third quarter of 2025, similar to the increases in the previous two quarters and the average quarterly increase of 1.0% in 2024. URA reported that 8 developers launched 4,191 uncompleted private residential units for sale in the third quarter of 2025, compared with the 1,520 units in the previous quarter and 9 developers sold 3,288 private residential units in the third quarter of 2025, compared with the 1,212 units sold in the previous quarter. To maintain market stability, the Government is sustaining a high level of private housing supply through the Government Land Sales ("GLS") Programme, with the total GLS Confirmed List supply of close to 10,000 units in 2025, or around 50% higher than the average annual Confirmed List supply from 2021 to 2023.

Despite uncertainties in macroeconomic factors, the investment properties and hotels held by the Group in Singapore and overseas have maintained satisfactory occupancy rates and rental rates.

The Group's construction order book remains healthy at more than S$500 million as at 13 November 2025.

As at 1HFY2026, the Group has four joint ventures for proposed residential and mixed redevelopment in Singapore. Namely The Arcady at Boon Keng, One Sophia/The Collective at One Sophia, Sora at Yuan Ching Road in District 22 and Bagnall Haus at 811 Upper East Coast. These projects have achieved satisfactory sales with expected positive margin since launch. Construction for these four projects have commenced. Based on options signed for the above-mentioned launched projects as at end September 2025, the Group's equity share of unrecognised attributable revenue on sold units was approximately S$168 million and will be recognised based on percentage of completion in accordance with the relevant construction progress.

In the PRC, the property market remains challenging although the Government's targeted stimulus efforts have helped improve buyer sentiment and confidence. The Group's two projects in Gaobeidian, Singapore Sino Health City – Zhong Xin Yue Lang ("ZXYL") and Zhong Xin Yue Shang ("ZXYS") continue to record sales.